Every digital activity leaves a physical trail. When you make a UPI payment, stream Netflix, back up WhatsApp, place a stock market trade or ask ChatGPT a question, that request travels to a data centre, where servers process it and send a response back in milliseconds. Once seen as the Internet’s invisible plumbing, data centres are now at the centre of a global infrastructure boom driven by AI, cloud computing and surging digital traffic.

The data centre industry uses an unusual convention: Although operators are effectively digital landlords renting out space and computing capacity, facilities are sized and marketed by the electrical power available to IT equipment, expressed in MW or GW of “IT load”, rather than by floor area, server count or data handled. Real estate consultant Knight Frank estimates data centre global live IT capacity at about 60 GW in 2025, rising to over 93 GW in 2027, while another consultant JLL sees as much as 100 GW of new capacity by 2030.

The global rush has been extraordinary, and data centres are changing with it. AI facilities need far more power, cooling and electrical infrastructure than older ones, as large language models can require 10-100 times the computing power of traditional applications. By 2030, AI could account for half of all computing activity, with running trained AI models driving most of it.

That template is now playing out in India too. Despite generating an estimated 20 per cent of the world’s digital data, our data centre market remains far smaller than those of the US or China, though it is among the fastest-growing, with capacity rising from about 0.375 GW in 2020 to around 1.5 GW by 2025 (estimated 130-150 active data centres). Mumbai and Chennai account for a lion’s share of installed co-location capacity today because of their proximity to sub-sea cable landing stations. Projections suggest a three-seven-fold rise in national capacity by 2030, to 4.5-10 GW. Hyperscalers (typically large cloud providers), such as AWS, Microsoft, Google and Oracle, already account for more than half of India’s data centre IT capacity, with BFSI and IT & Telecom being the other major clients.

Below, we unpack data centre evolution, business, economics and opportunities.

Brief history of data centres

Data centres have evolved in step with the changing needs of computing. Their origins can be traced to the 1940s and 1950s, when early mainframe computers were so large and power-intensive that they required dedicated rooms with specialised cooling. One of the earliest examples was the U.S. Army’s ENIAC, completed in 1945 at the University of Pennsylvania.

In the 1960s and 1970s, as businesses increasingly adopted mainframe systems, dedicated computer facilities became more common. IBM helped accelerate this shift in the 1970s by developing standardized sites for its mainframe machines, supporting the growing need for large-scale data processing.

The 1980s marked a major transition with the rise of client-server architecture. Organizations now needed separate spaces not only for servers but also for networking equipment, laying the groundwork for the modern data centre as IT resources became more centralized.

Demand expanded sharply in the 1990s with the growth of the internet. Companies needed reliable infrastructure to host websites and run online services, leading to rapid expansion in data centre capacity.

In the 2000s, virtualization improved server utilization and helped pave the way for cloud computing. Data centres became more scalable and flexible, transforming how businesses deployed infrastructure and managed digital operations.

The 2010s saw the emergence of hyperscale data centres built to handle the massive processing and storage needs of technology giants. At the same time, edge computing began gaining ground by moving processing closer to users, helping reduce latency and improve performance.

In the 2020s, data centres are being reshaped again by artificial intelligence, which demands far greater computing power. Alongside this, sustainability has become a central priority, with operators focusing more on reducing energy use and lowering environmental impact.

Not just a building of servers

A visit to a modern data centre feels less like entering an office and more like entering a military facility: Armed guards, multiple biometric checks and man-trap doors outside, followed by long, deafening corridors of blinking server racks, thick cables and icy air inside.

At its core, a modern data centre is five things rolled into one. A secure building that houses servers and storage, a private electricity system with multiple layers of backup, a cooling system designed to remove huge amounts of heat, a network hub connected to fibre-optic cables and the wider Internet, and computing power from central processing units (CPUs), graphics processing units (GPUs), and specialised chips.

According to BofA Global Research, IT equipment (servers, networking, storage) accounts for 79 per cent of the cost, followed by engineering, contractor, building and installation costs (E&C) at 11 per cent, electrical equipment at 5 per cent, thermal or cooling equipment at 4 per cent and backup diesel generators at 1-2 per cent.

Traditional data centres are built on-site and expanded gradually, making them slower to deploy but more customisable. Modular facilities, by contrast, use prefabricated units that can cut construction time from roughly 18-24 months to 6-12 months.

But the faster data centres scale, the harder it becomes to ignore their side-effects. Beyond land and capital, these facilities place heavy demands on power grids, water resources and local infrastructure.

Different models

Data centres can broadly be understood through four models, though these categories often overlap.

Captive or enterprise data centres are owned and run by a company for its own workloads. A bank, stock exchange or large enterprise may prefer this route for tighter control over security, compliance and design. The trade-off is high capex, lower flexibility and the burden of managing power, cooling and security in-house.

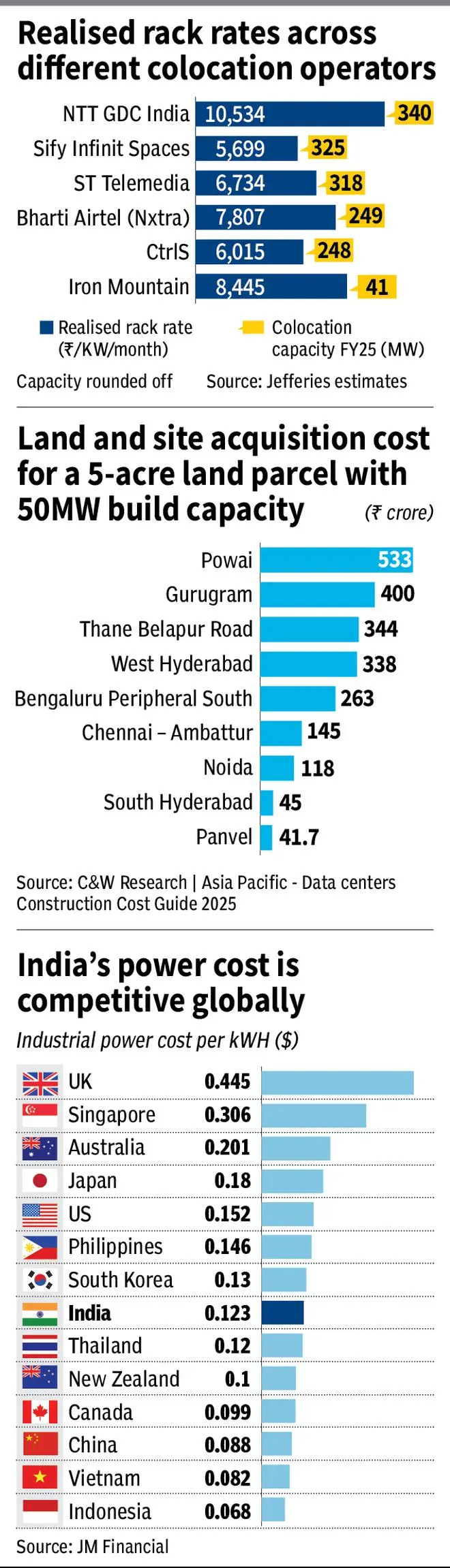

Co-location (colo) data centres are shared facilities where multiple customers rent space, power and connectivity from an operator such as Equinix or Digital Realty. They reduce upfront costs and improve scalability but offer less control than captive set-ups and leave users dependent on operator uptime and pricing. In India, the average colo capex per MW in India is ₹46.5 crore/$5.4 million and this works out to roughly ₹24,200 of capex per sq ft, per JM Financial. Research by Soben (part of Accenture) found that cloud data centres currently cost between $8 million and $10 million per MW, GW+AI data centres are costing as much as $17 million per MW. This gap reflects differences in scope, geography, design assumptions, and included IT and hardware.

Hyperscale data centres refer more to size and intensity than ownership. These are giant campuses built for cloud majors such as Amazon, Microsoft, Google and Meta, either for their own use or through leased capacity from operators. They can range from several dozen MW to 100 MW-plus at a site level, with some campuses planned at far larger scale. They deliver scale and efficiency, but require huge power, land and capital. A newer variation of this buildout is CoreWeave, which is closer to an AI-focused leased-infrastructure model built around GPU cloud workloads.

Edge data centres are smaller, decentralised facilities placed closer to users and devices, often below 10 MW in India, including in smaller cities and towns. Telecom operators use such set-ups to cut latency and support real-time applications, though these sites usually offer lower redundancy and uptime than large centralised facilities.

Interestingly, recent attacks on data centres and digital infrastructure during the Middle East conflict have revived interest, at least in theory, in underground and even space-based facilities. But both remain prohibitively expensive: underground campuses can cost 1.5-2 times as much as conventional ones, while Deutsche Bank Research estimates a 1 GW space data centre would cost at least seven times more than a terrestrial one.

Business economics

Data centres generate revenue through pricing models based on rack units (server slots), full racks (entire cabinets), cages (private enclosed areas) and other formats, with pricing increasingly linked to the amount of power allocated to them. Rates depend on location, power availability, network density, uptime, security and contract structure. Pricing can also vary by customer size, ranging from retail users taking under 0.25 MW to hyperscalers taking above 4 MW.

Retail and wholesale colo contracts typically run for three-five years, while hyperscaler deals usually last at least five years and can extend to 10.

Broadly, there are two revenue models. In the dominant lease model, the data centre operator rents out space, power and cooling, while the customer manages its own IT infrastructure. In managed services, the operator also provides cloud or IT infrastructure and charges on a usage basis. In India, lease rentals can be around ₹10-11 crore per MW per year, with utilities typically passed through separately.

Besides pricing and capacity, a data centre’s profitability depends on occupancy and cost control.

In India, colo occupancy has climbed sharply, from 82 per cent in FY20 to 97 per cent in FY25. With facilities now running at 95-97 per cent occupancy, fresh capacity additions are becoming increasingly critical.

On pricing, the most useful current benchmark is realised rack rate, which Jefferies estimates at an aggregate ₹7,428 per kW per month in FY25. Monthly pricing, typically, falls as customer size rises.

Power is the single-most vital resource for data centre operations and a critical factor in financial viability. Thanks to renewable power, India is not short of electricity in aggregate. But that does not automatically mean every location has easy, reliable and scalable access to it. Tariff classification matters, since data centres usually seek industrial power rates, which can be materially lower than commercial tariffs.

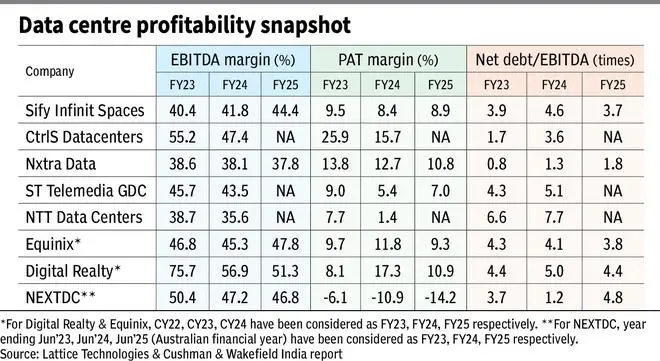

Change in energy costs can hit or benefit reported EBITDA margins (FY25: of 37-44 per cent for players in India and 47-51 per cent for global firms). Power density has increased thanks to GPUs, which are now central to modern computing, especially in AI, data analytics, and high-performance computing. For context, NVIDIA H100 and H200 GPU-based racks typically draw about 10-30 kW each, marking a sharp jump from legacy enterprise densities. While traditional racks used about 12 kW, AI-ready racks can require 80-120 kW for training. For understanding, a single 100 kW AI rack running 24/7 in India (at ₹8-10 per unit/kWh) would cost ₹6-7 lakh per month just in electricity, before cooling or floor space costs.

Data centres try to lower power costs through a mix of efficiency, technology and location strategy. Improving Power Usage Effectiveness (PUE) can materially cut energy bills; a 0.1 reduction in PUE can save about ₹10 crore annually for a 20 MW facility. Operators are also using AI to optimise cooling and power distribution in real time.

Long-term renewable power purchase agreements (PPAs), too, help lock in lower energy costs. Some States offering electricity-duty waivers or concessional tariffs make certain locations more attractive.

Data centres are also highly capital-intensive businesses, with large upfront spending. McKinsey research shows that by 2030, data centres are projected to require $6.7 trillion worldwide to keep pace with the demand for compute power. Data centres equipped to handle AI processing loads are projected to require $5.2 trillion in capex, while those powering traditional IT applications are projected to require $1.5 trillion. This makes financing costs crucial.

Debt is a standard part of funding expansion, whether for construction, fit-outs or ongoing operations. Interest costs can materially affect margins, especially when operators add capacity aggressively before utilisation ramps up. Reported net debt/EBITDA ratios for major operators range from under two times for some players to above five-seven times for more leveraged ones, with global Real Estate Investment Trust (REIT)-like players often in the 3.8-4.4 times range. In the asset-intensive data centre industry, depreciation can be a key swing factor. High depreciation in the early years of capacity expansion tends to depress EBIT, ROCE and PAT, but as utilisation improves and revenues scale up, its relative impact usually falls.

Given the growth potential, the sector is attracting institutional capital from private equity, pension funds, REIT-like vehicles and global strategic partners. According to industry estimates, India’s data centre market has attracted nearly $94 billion in investments since 2019. For instance, Airtel on March 30 announced a $1-billion investment in its subsidiary Nxtra, which operates 14 large core data centres and 120+ edge facilities, by Alpha Wave, Carlyle and Anchorage Capital, with Airtel also participating. In November 2025, Tata Group’s TCS partnered with PE giant TPG to scale HyperVault, targeting over 1 GW of AI-ready data-centre capacity with investments of up to ₹18,000 crore (about $2 billion).

Bigger conglomerates have also unveiled ambitious plans this year. Adani Group plans to invest $100 billion by 2035 in renewable-powered, AI-ready data centres, backed by a parallel scale-up in renewable energy and storage. Reliance has outlined a $110-billion, seven-year AI infrastructure plan spanning gigawatt-scale data centres, a nationwide edge-computing network and AI services integrated with Jio.

Data centre value chain

A data centre draws on a wide vendor ecosystem.

The server layer includes the likes of Dell and Hewlett Packard, while networking gear comes from Cisco, Arista Networks and Juniper Networks. The electrical backbone spans UPS systems, switchgear, power distribution units (PDUs), with vendors such as Schneider Electric, Vertiv, Eaton and ABB. The cooling stack includes chillers from firms such as Johnson Controls, Trane, Carrier and Daikin; heat-rejection equipment such as cooling towers, dry coolers and related systems from SPX Technologies, Ebara and Kelvion; and computer room air handlers (CRAHs) from Vertiv, STULZ and Johnson Controls. Back-up power comes from suppliers such as Caterpillar, Rolls-Royce mtu and Cummins. Large projects also rely on engineering and design firms such as Jacobs, Burns & McDonnell and WSP, along with construction specialists such as Turner, Holder and HITT.

In India, the value chain spans multiple listed and unlisted players. E2E Networks, as a specialised AI-cloud provider, competes with AWS, Microsoft Azure and Google Cloud. Cooling needs create opportunities for Voltas, Blue Star and Hitachi. The telecom opportunity is served by Reliance Jio, Bharti Airtel, Tata Communications etc. The electrical and power layer is served by firms such as Hitachi Energy India, ABB India, Siemens Energy, Schneider Electric and CG Power, while cables/switchgear names such as Polycab, KEI, Havells are also often cited. Land, shell and real-estate development involve players such as Brookfield, Blackstone, Embassy and Lodha. Some, such as Anant Raj, are using their existing land banks through Anant Raj Cloud to build AI-ready data centres. Racks, fit-outs and project execution draw in Larsen & Toubro, Sterling and Wilson, NCC etc.

India has one major advantage in the global race: cost. The policy push is also strengthening. Budget 2026 proposed a 20-year tax holiday, till 2047, for eligible foreign cloud companies using Indian data centres for global operations. This adds to a broader regulatory tailwind from the RBI’s 2018 payments-data localisation mandate, MeitY’s Data Centre Policy 2020, SEBI’s 2023 data-in-India rule for regulated entities, the DPDP Act 2023 and the IndiaAI Mission 2024.

Yet India’s expansion is not frictionless. A new data centre requires close to 30 approvals or permissions from Central and State government departments before it can start operations. Land acquisition can be slow. Grid connections may take time. Even if India does not face an overall national power shortage, the availability of reliable electricity varies sharply across cities and sites. The biggest challenge may, therefore, be execution.

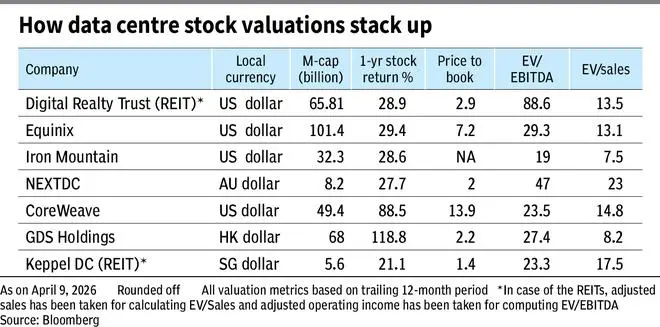

Unlike Digital Realty, Equinix, NEXTDC, CoreWeave, GDS Holdings and Keppel DC REIT etc., none of the pure-play data centres are listed in India till now. Sify’s data centre business (Sify Infinit Spaces) may be the first to list.

Investors should understand that in the builder-operator model, cash flows are back-ended. Operators spend heavily on land, power infrastructure and construction long before utilisation matures, so near-term free cash flow can look weak even if the underlying asset is attractive. Large builds can be EBITDA-negative or cash-flow negative until utilisation ramps, which is one reason private capital often dominates the sector. Globally, companies such as CyrusOne, QTS Realty, Switch and Chindata are prominent examples of data centre firms that were once publicly listed but were later taken private.

How to assess the theme

The pros for data centre investors are long-duration demand, sticky customers, high switching costs and rising value for power-rich, well-connected campuses. The cons include huge upfront capital needs, long gestation, execution risk on power and approvals, and uncertain returns if too much capacity is built at once.

A data centre REIT may generate steady rental income, but because it distributes most of its cash flows, future growth often has to be funded through fresh debt, equity issuance or asset sales.

Some investors, especially in India, may see the opportunity as a classic “during a gold rush, sell shovels” story. But a list of “data centre stocks” and projected spending is not an automatic way to successfully ride the boom. Investors still need to judge how seriously each company is targeting the opportunity in India and overseas, what the management says on con-calls, whether order-wins are translating into revenue and whether margins are attractive enough to matter.

For active investors, the checklist should vary by segment.

In power and electrical equipment, assess product relevance, execution capability, order inflow, margin profile and competitive intensity.

In cooling, check whether the company has genuine data-centre-grade capability or is merely using the theme as a narrative.

In construction and fit-outs, study project scale, EPC execution, working-capital demands and margin sustainability.

In telecom and fibre, understand whether data centre demand can materially lift utilisation and returns.

Across all names, investors need to judge whether the exposure is real and scalable, whether it can materially improve profits, and whether valuations already price in too much optimism.

Published on April 12, 2026

Source link

#AWS #Microsoft #Google #Adani #Reliance #driving #Indias #data #centre #boom