AlphaStreet Newsdesk powered by AlphaStreet Intelligence

FY26 EPS guidance – adjusted $0.35 – $0.41|Stock $6.31 (+0.0%)

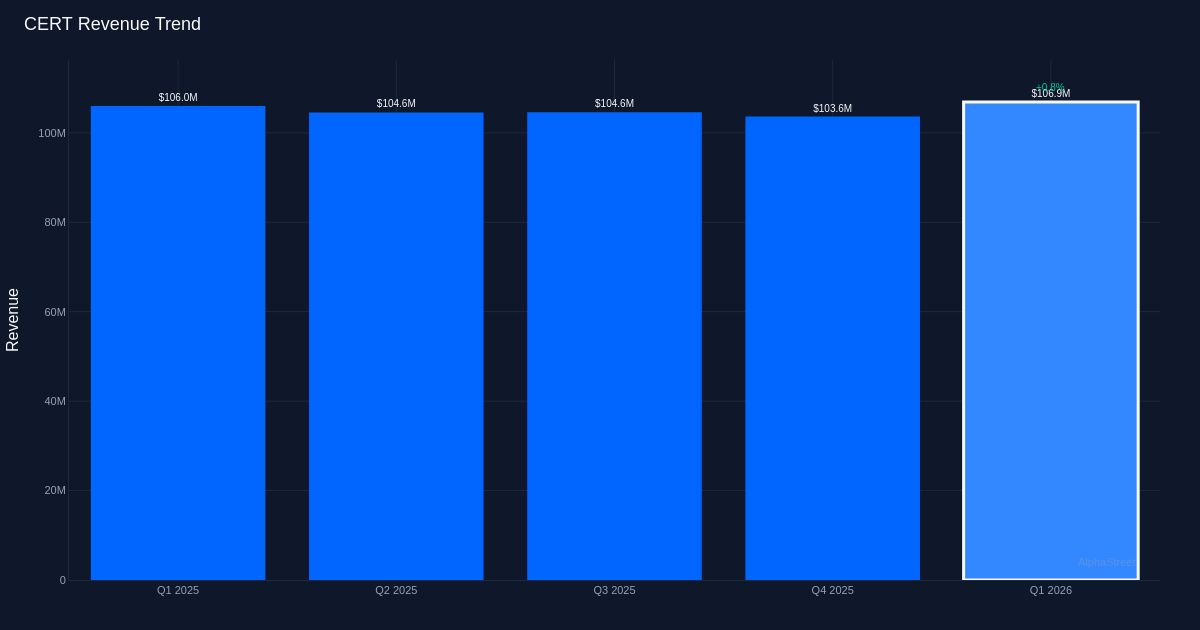

Mixed Quarter. Certara, Inc. (NASDAQ: CERT) delivered a split performance in Q1 2026, with adjusted EPS of $0.09 missing the $0.11 consensus estimate by 18.2% based on estimates from 11 analysts, while revenue of $106.9M edged past the $106.1M consensus by 0.8%. The health information services provider posted adjusted net income of $14.5M. The stock traded largely unchanged following the report, suggesting investors had already braced for execution challenges.

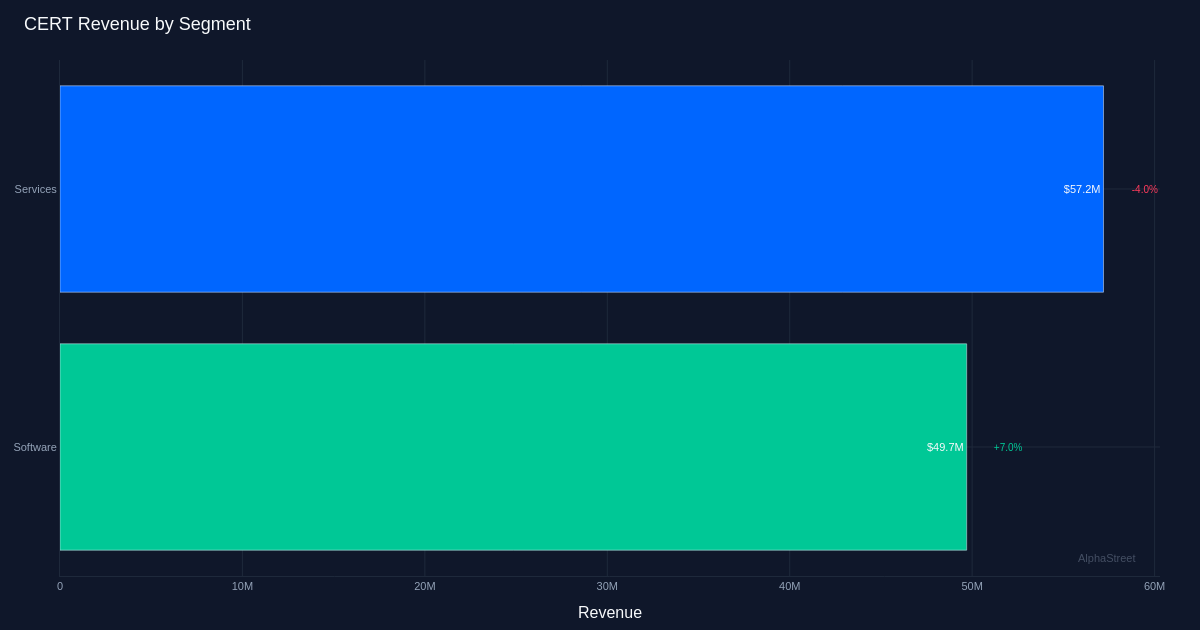

Muted Revenue Growth. The 1.0% year-over-year revenue expansion reflects sluggish demand dynamics in Certara’s end markets, though the company did manage to exceed consensus by a narrow margin. Total Bookings reached $115 million for the quarter, a metric that will be critical to monitor for signs of future revenue acceleration. The earnings miss appears driven more by cost structure issues than revenue shortfalls, given the top-line beat, which raises questions about operating leverage in the current environment. Software emerged as the clear standout, generating $49.7M in revenue with 7.0% year-over-year growth, demonstrating that at least one segment is gaining traction despite broader headwinds.

Guidance Provides Limited Comfort. Management projected FY 2026 adjusted EPS in the $0.35 to $0.41 range, while revenue is expected to land between $395.0M and $405.0M. The wide range on both metrics suggests meaningful uncertainty around the company’s ability to accelerate growth or improve margins through year-end. If the quarter’s 1.0% growth rate persists, Certara would need a substantial pickup in the remaining three quarters to reach even the midpoint of its revenue guidance. The EPS outlook, meanwhile, implies significant margin improvement must materialize in coming quarters to offset the Q1 shortfall.

Investor Sentiment Neutral. Wall Street maintains a cautiously balanced view with analyst consensus at 7 buy ratings and 9 hold ratings, with no sell recommendations. This split reflects the tension between Certara’s long-term positioning in biosimulation software and near-term execution challenges. The largely unchanged stock price following results indicates the market is adopting a wait-and-see posture, unwilling to either abandon the story or reward management until clearer evidence of inflection emerges.

What to Watch: The path to management’s full-year guidance hinges on whether Software’s 7.0% growth can broaden across other segments and whether Total Bookings momentum builds through Q2, providing visibility into the second-half acceleration required to meet revenue targets while simultaneously delivering the margin expansion implied by the EPS range.

This content is for informational purposes only and should not be considered investment advice. AlphaStreet Intelligence analyzes financial data using AI to deliver fast and accurate market information. Human editors verify content.

Source link

#Certara #Falls #Short #EPS #Expected #Alphastreet