Q1 2026 Deep Dive: .25 Loss; Revenue Surges – Alphastreet")

AlphaStreet Newsdesk powered by AlphaStreet Intelligence

Stock $7.76 (+4.3%)

plans. Should workers embrace them?")

EPS YoY -76.6%

|

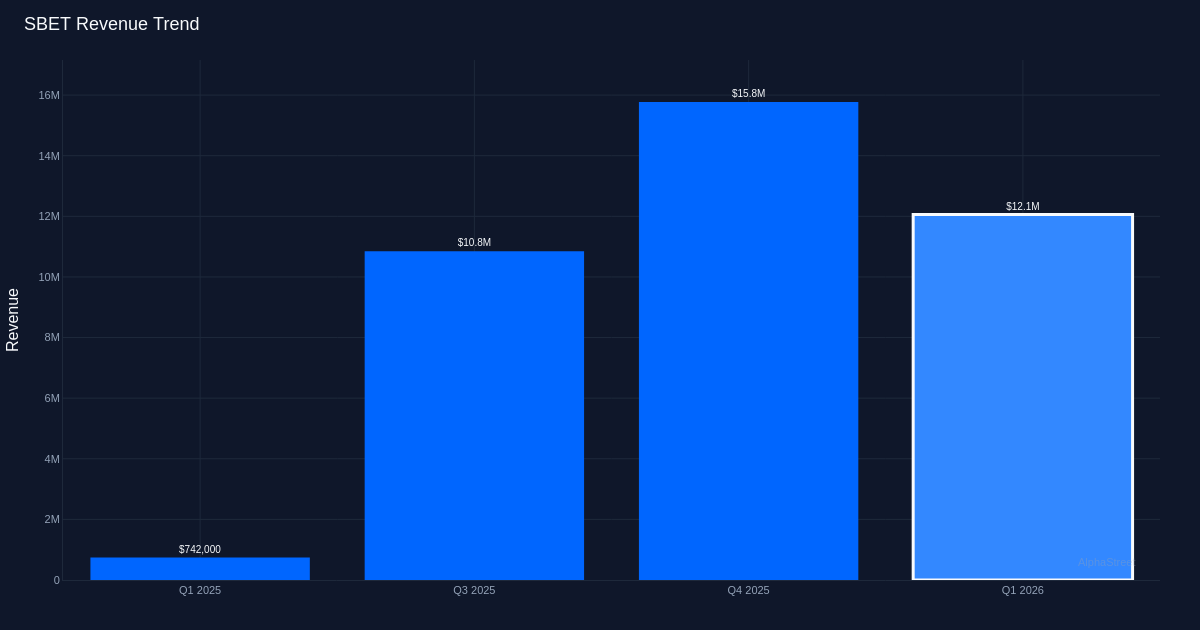

Sharplink (SBET) delivered a Q1 2026 earnings miss, reporting a loss per share of $3.25 against analyst expectations of a $0.01 loss—a miss that raises fundamental questions about the company’s business model viability despite explosive revenue growth. The capital markets firm posted $12.1 million in revenue, marking a sharp year-over-year growth, yet managed to burn through $685.6 million in net losses during the quarter. The stock’s 4.3% uptick to $7.76 suggests investors are focusing on the revenue trajectory rather than the alarming deterioration in profitability.

The quality of Sharplink’s growth is deeply troubling, with operating leverage moving in the wrong direction at scale. Management acknowledged the cost explosion, noting “SG&A expenses in the first quarter were $9.9 million compared to $1.1 million in the prior year quarter,” but the nine-fold increase in operating expenses doesn’t explain the 700-fold increase in net losses. The math points to significant non-operating charges or asset impairments that management has not fully disclosed in available commentary.

Profitability trends across recent quarters paint a picture of extreme instability rather than growth-stage predictability. The wild swings in recent quarters —from profitable to massively unprofitable and back—indicate either exceptional revenue quality issues or substantial one-time charges that aren’t being clearly communicated. Management’s comment that “net loss for the quarter ended March 31, 2026 was $685.6 million versus $1 million loss in the prior year” states the fact but offers no explanation for the 685x deterioration.

Management’s strategic pivot toward tokenized real-world assets and liquid restaking suggests an attempt to ride emerging crypto infrastructure trends, but the connection to current financials remains opaque. The commentary that “in January we took a portion of our portfolio around 8% and we put it in a composable liquid restaking token alongside Consensus, Linea, Etherfi and Eigencloud” indicates active treasury management of the substantial ETH position, but provides no clarity on how this generated $12.1 million in quarterly revenue or produced a $685.6 million loss. The observation that “to date there’s about 30 to 35 billion of on chain real world assets that have been tokenized” positions Sharplink in a growing market, but without disclosure of the company’s market share, revenue model, or unit economics in this space, investors are left connecting dots without sufficient data points.

The earnings miss comes against minimal analyst coverage and expectations, with the company posting a 0% beat rate over the last quarter of reported results. The fact that consensus expected a near-breakeven quarter at a $0.01 loss while the company delivered 325x that loss suggests either a catastrophic breakdown in guidance communication or analysts working with incomplete information about the business model. For a financial services firm in capital markets, this level of forecasting disconnect is particularly problematic, as it suggests the revenue and expense drivers are neither transparent nor predictable.

The positive stock reaction despite the massive earnings disappointment indicates the market is either pricing in asset value from the ETH holdings rather than operating performance, or viewing the revenue growth as validation of a viable business emerging from development stage. At $7.76 per share with 4.02 ETH per share in holdings, investors appear to be assigning enterprise value based on the cryptocurrency concentration rather than traditional earnings multiples. This creates a hybrid valuation framework where Sharplink trades partly as a levered bet on Ethereum and partly as a capital markets platform, but the 4.3% gain suggests the former is driving sentiment more than operating fundamentals.

What to Watch: Management must provide detailed reconciliation of the $685.6 million net loss, breaking out operating losses from any asset impairments or mark-to-market charges on the ETH portfolio. The sustainability of the revenue model needs clarification—specifically whether the $12.1 million represents recurring platform fees, transaction-based revenue, or gains from treasury management. Sequential revenue trends in Q2 will reveal whether Q1’s decline from Q4 was seasonal or structural. Finally, investors need transparency on the company’s cash burn rate and runway given the magnitude of losses, along with any hedging strategy for the concentrated Ethereum exposure that represents over half the market capitalization on a per-share basis.

This content is for informational purposes only and should not be considered investment advice. AlphaStreet Intelligence analyzes financial data using AI to deliver fast and accurate market information. Human editors verify content.

Source link

#Sharplink #SBET #Deep #Dive #Loss #Revenue #Surges #Alphastreet