Goldman Sachs has slashed India’s growth forecast by 50 basis points, flagging the West Asia conflict as a fundamentally different kind of oil shock – one that strikes both ends of India’s economic exposure to the region simultaneously and could push the rupee to 95 against the dollar within a year.

Santanu Sengupta, Goldman Sachs’s MD and Chief India Economist, outlined the firm’s detailed scenario on Now – one built on a base case of a 21-day Strait of Hormuz closure, oil at roughly $100 during that window, and a gradual retreat toward $85 in April and the $70s by the second half of the year.

Why this oil shock is different from the last 25 years

India has absorbed energy price shocks before, but Sengupta stresses this episode carries a structural twist that makes it harder to navigate. In every prior cycle, rising oil prices enriched Middle Eastern economies – and India benefited indirectly through stronger export demand from the region and higher remittances flowing home. That offset no longer exists.

This time the conflict is located in the Middle East itself. Their economies will be doing worse than in the past – and India is far more integrated with that region than it was 10 or 15 years agoSantanu Sengupta, Goldman Sachs

The scale of that integration is striking. Sengupta put precise numbers to India’s exposure to the region – figures that explain why the simultaneous hit to exports, energy imports, and remittances makes this shock qualitatively different from earlier ones.

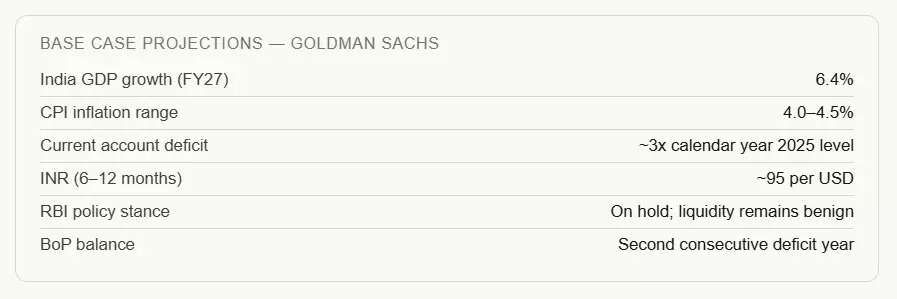

Goldman’s base case scenario: Growth, inflation, and currency

The firm’s central forecast rests on an assumption that fiscal policy absorbs most of the domestic shock – mirroring the playbook used during the 2022 commodity cycle, when the government raised fertiliser subsidies by 50 basis points of GDP and kept petrol and diesel pump prices steady through a combination of OMC absorption and excise duty cuts.

Under this framework, Sengupta does not expect the RBI to raise rates – inflation is moving from a very low base of 2-2.5% and the growth shock is seen as the bigger near-term concern. The central bank is expected to stay on hold and continue injecting liquidity through open market operations to offset any FX-related drain.

The rupee and external balances: Limited protection available

While fiscal tools can shield domestic growth and inflation to a meaningful degree, Sengupta is explicit that the external account cannot be managed the same way. India’s current account deficit is projected to widen to roughly three times its calendar year 2025 level, and a second consecutive year of balance of payments deficit now looks probable.

India enters this shock from a position of relative strength – external debt is low as a share of GDP and foreign exchange reserves stand above $700 billion. But with the flow environment deteriorating and remittances under pressure, the rupee is expected to slide from current levels of around 92 toward 95 over the next six to twelve months.

If the crisis drags on: Fiscal stress and a potential policy shift

Sengupta maps out what happens if oil stays above $100 beyond a quarter or more. The government’s ability to absorb the shock fiscally – keeping pump prices steady and covering fertiliser costs in full – comes under growing strain. At some point, a pass-through to consumers becomes unavoidable. If that happens, the calculus for the RBI changes materially: inflation could overshoot, and rate action later in the year cannot be ruled out.

On near-term demand management, the government has already activated the Essential Commodities Act to prioritise household cooking gas over industrial use. Goldman views this as the right call for protecting lower-income households, even though it introduces some risk to industrial output during the disruption period.

The bottom line from Goldman Sachs: India’s macroeconomic buffers are real and meaningful, but this shock has more tentacles than any comparable episode in the past two decades. How long crude stays elevated – and whether the government can hold the fiscal line – will determine how much of that 50-basis-point growth cut ultimately sticks.

Source link

#Goldman #Sachs #cuts #Indias #growth #forecast #FY27 #sees #sliding #Santanu #Sengupta #full #outlook