AlphaStreet Newsdesk powered by AlphaStreet Intelligence

Stock $165.64 (+0.7%)

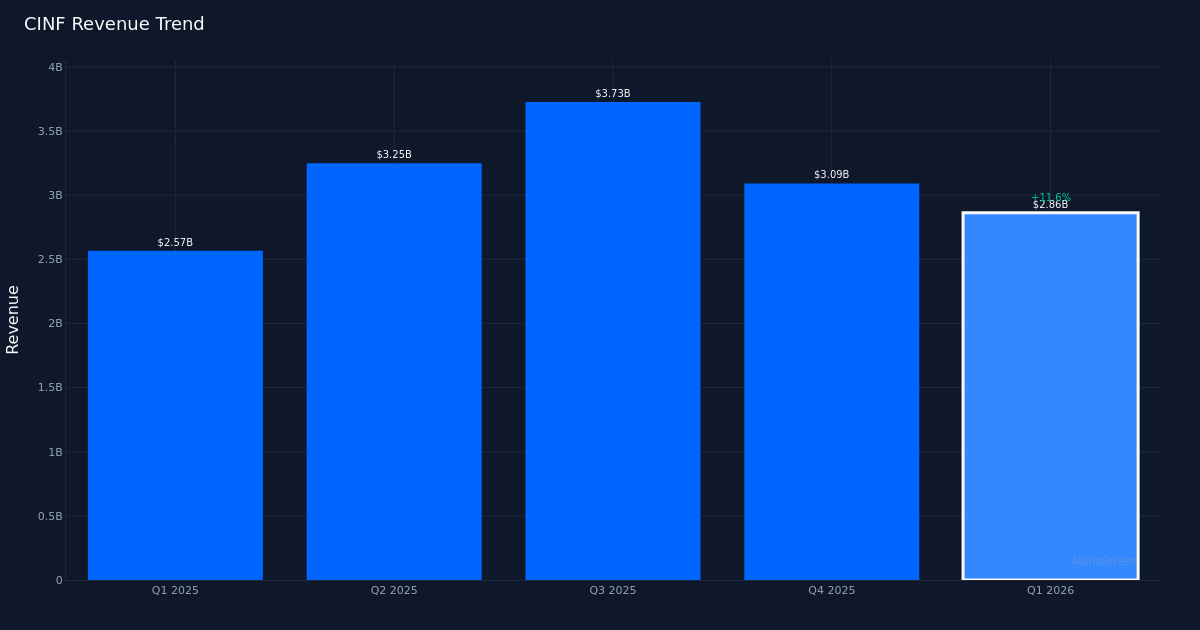

Solid beat. Cincinnati Financial Corporation (NASDAQ: CINF) delivered Q1 2026 non-GAAP operating income of $2.10 per share, surpassing the $1.99 Wall Street consensus by 5.5%. Revenue totaled $2.86B for the quarter, up 11.6% from $2.57B in Q1 2025, demonstrating momentum across the property and casualty insurer’s core business lines. Net income reached $330.0M for the quarter, while the stock traded largely unchanged following the release, suggesting investors had already priced in much of the positive performance.

Underwriting discipline shines. The combined ratio came in at 95.6% for the quarter, reflecting the company’s continued underwriting proficiency in a competitive market. A combined ratio below 100% indicates underwriting profitability before investment income, a critical metric for gauging operational excellence in the property and casualty insurance sector. This disciplined approach to risk selection and pricing appears to be driving the quality of the earnings beat, rather than relying solely on expense reductions or one-time benefits.

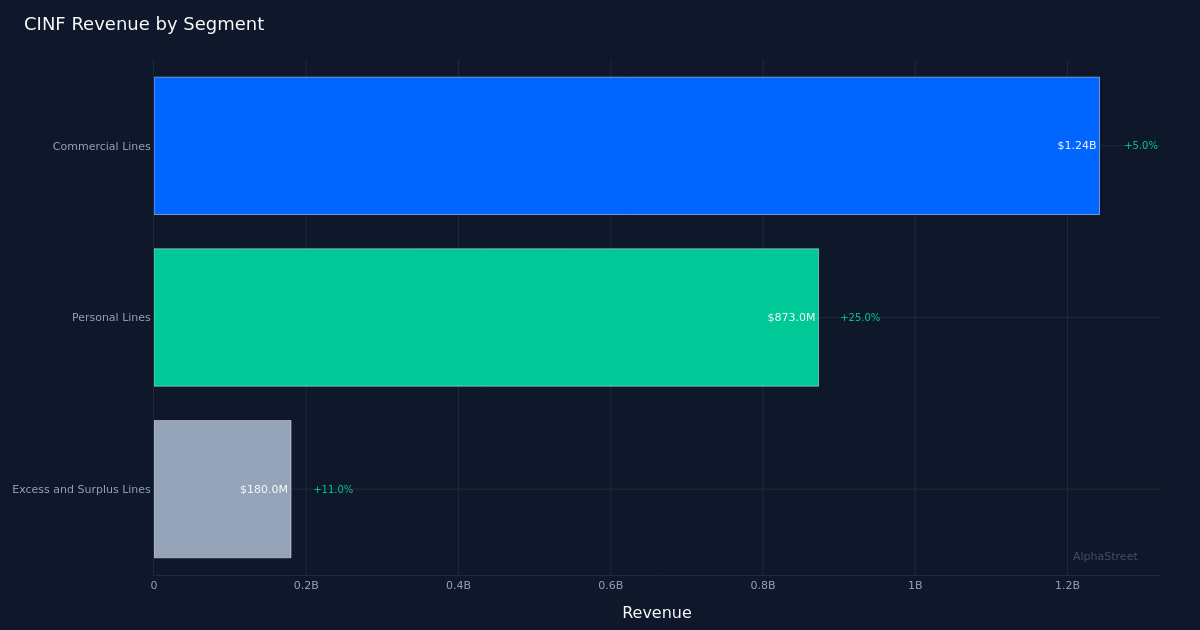

Commercial strength drives growth. Commercial Lines led segment performance with $1.24B in revenue, up 5.0% year-over-year, underscoring the strength of Cincinnati Financial’s core franchise with independent agents. The double-digit revenue growth at the company level suggests broad-based momentum beyond just the Commercial Lines segment, pointing to successful execution across Personal Lines and other offerings. The company operated 108 new agency appointments at quarter end, expanding its distribution footprint and positioning the insurer for continued premium growth.

Revenue-driven performance. The 11.6% year-over-year revenue expansion indicates this earnings beat stems from genuine top-line momentum rather than aggressive cost-cutting measures. For insurers, revenue growth combined with a sub-96% combined ratio represents a particularly attractive dynamic, as it demonstrates the ability to grow the business while maintaining underwriting discipline. This quality of beat should resonate with institutional investors focused on sustainable earnings power rather than short-term margin manipulation.

Analyst confidence persists. Wall Street consensus stands at 7 buy ratings and 5 hold ratings with 0 sell recommendations, reflecting generally positive sentiment toward the company’s prospects. The muted stock reaction despite the beat suggests the market may be waiting for additional catalysts or confirmation that the growth trajectory can be sustained through the remainder of 2026. The lack of negative sell-side ratings indicates analysts see limited downside risk from current levels.

What to Watch: Focus on whether Cincinnati Financial can maintain its sub-96% combined ratio while continuing to expand agency relationships throughout 2026, as sustained underwriting profitability alongside distribution growth would validate the premium valuation multiples typical of best-in-class property and casualty insurers.

This content is for informational purposes only and should not be considered investment advice. AlphaStreet Intelligence analyzes financial data using AI to deliver fast and accurate market information. Human editors verify content.

Source link

#Cincinnati #Financial #Delivers #Revenue #Growth #Alphastreet