AlphaStreet Newsdesk powered by AlphaStreet Intelligence

Stock $46.97 (+8.2%)

EPS YoY +682.4%|Rev YoY +11.9%|Net Margin 5.1%

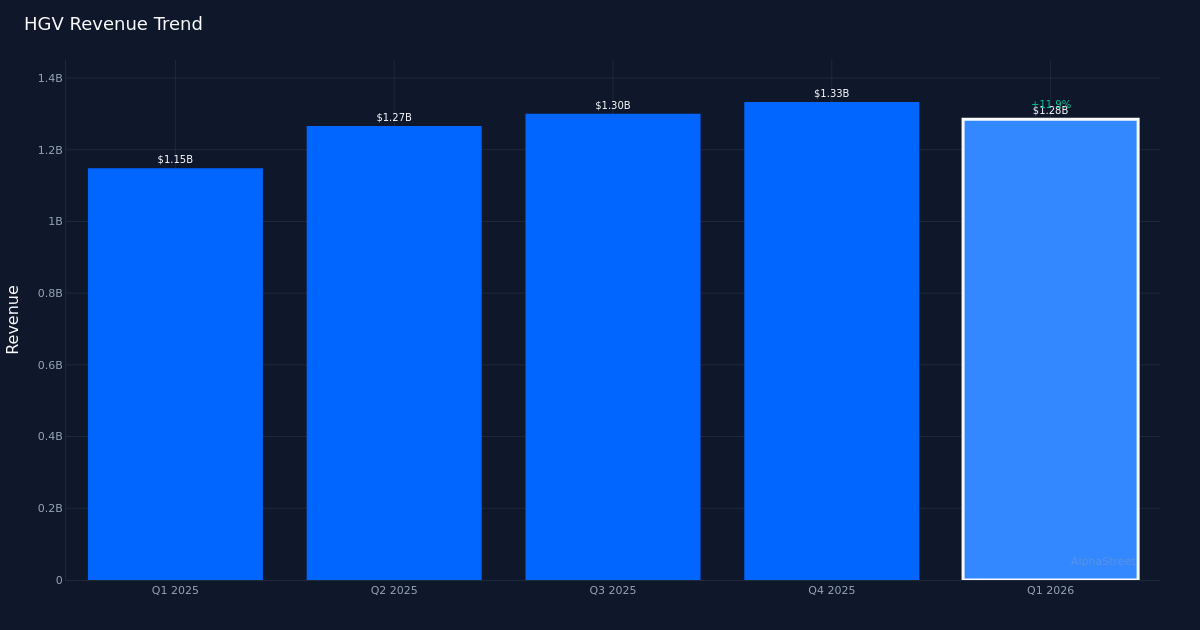

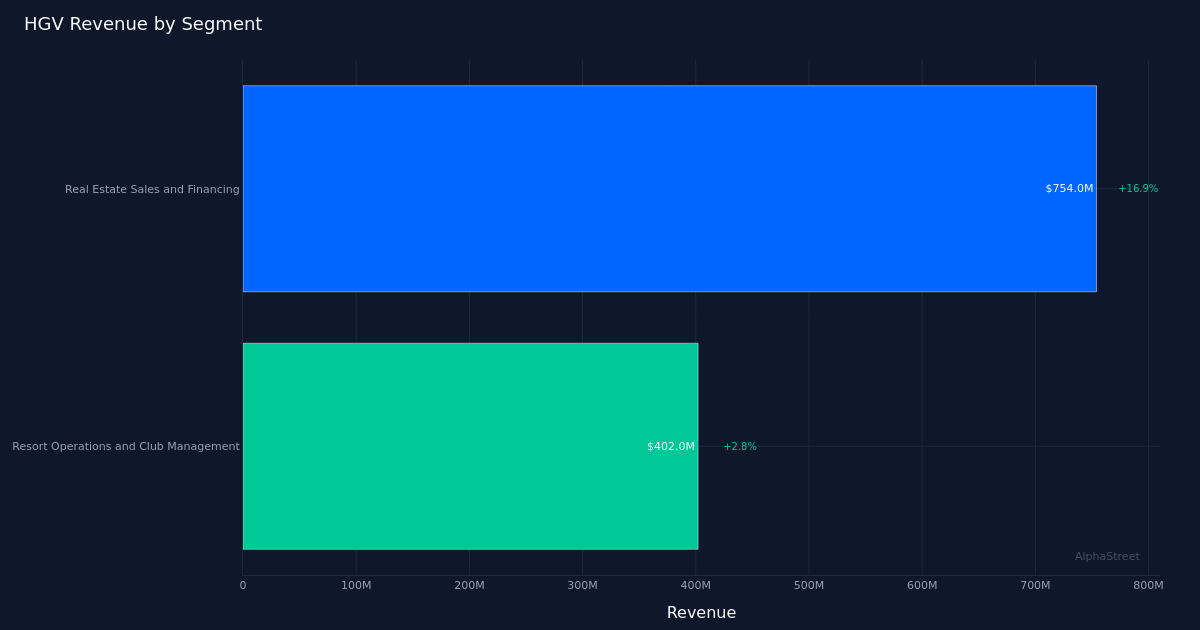

Hilton Grand (HGV) Vacations delivered a commanding earnings surprise in Q1 2026, crushing analyst expectations by 90.4% with adjusted EPS of $0.99 versus the $0.52 consensus. The $1.28B in revenue represented 11.9% year-over-year growth, driven primarily by the Real Estate Sales and Financing segment which expanded 16.9% to $754.0M. This wasn’t merely a beat—it marked a dramatic reversal from the year-ago loss of $0.17 per share.

The quality of this earnings performance shows through in the margin expansion story, where net margin surged from just 0.8% a year ago to 5.2% in the current quarter. That 4.4 percentage point improvement, combined with net income climbing to $66.0M, demonstrates this wasn’t a revenue-inflating exercise at the expense of profitability. EBITDA reached $249.0M while free cash flow generation hit $108.0M, providing the company with operational flexibility that was notably absent in the prior year period. The simultaneous expansion of both top-line growth and bottom-line margins reveals genuine operating leverage rather than financial engineering.

The revenue trajectory analysis reveals an inflection point worth examining closely, as Q1’s $1.28B represents the second-highest quarterly revenue in the trailing four quarters despite a sequential decline from Q4’s $1.33B. The pattern shows Q4 2025 at $1.33B, Q3 2025 at $1.30B, Q2 2025 at $1.27B, and Q1 2026 at $1.28B—a mixed trend that suggests seasonal variability rather than sustained momentum. However, the earnings trajectory tells a more compelling story: EPS progression from $0.25 in Q2 2025 to $0.28 in Q3, then $0.55 in Q4, and now $0.99 in Q1 2026 demonstrates accelerating profitability even as revenue plateaued. This divergence between revenue growth and earnings acceleration reinforces that margin improvement, not just scale, is driving shareholder value creation.

Segment dynamics reveal a tale of two businesses operating at markedly different velocities. The Real Estate Sales and Financing segment’s 16.9% growth to $754.0M accounted for nearly 59% of total revenue and clearly shouldered the growth burden, while Resort Operations and Club Management segment expanded just 2.8% to $402.0M. This bifurcation matters because it concentrates risk in the capital-intensive, cyclically-sensitive real estate sales business while the higher-margin recurring revenue from resort operations lags. Management acknowledged pricing pressure in one area, noting that “VPG was nearly $3,800 for the quarter, declining 8% and in line with the expectations of a high single digit decline we discussed last quarter,” suggesting that while volume may be growing in real estate sales, pricing power has moderated.

The membership base of 720,079 total club members provides an installed base for recurring revenue, though management’s emphasis on portfolio balance offers nuanced insight. As management noted, “… we have a very consistently strong performing portfolio, and if you think about the balance of the portfolio, it’s increased year over year by almost 8%.” This portfolio expansion appears to be supporting the contract sales figure of 719.0 million, though the relatively modest 2.8% growth in Resort Operations suggests that monetization of the member base hasn’t kept pace with real estate sales momentum. The credit quality commentary provides some reassurance, with management stating “their early, early-stage delinquencies that 0 to 30 day mark is actually at a 4-year low and has improved 11% subsequent to even quarter end,” which matters given the financing component of the business model.

The 8.2% stock price surge to $46.97 following the earnings release represents a rational response to the magnitude of the EPS surprise and the margin expansion demonstration. The market is rewarding not just the beat, but the fundamental shift from near-breakeven profitability a year ago to sustainable margin generation today. However, investors should recognize that much of the operational improvement may now be priced in, making the company’s ability to maintain this profitability trajectory while navigating pricing pressure in the VPG metric critical to sustaining the valuation.

The 100% beat rate over the last quarter establishes a limited track record, making consistency the key metric to establish credibility. One quarter of outperformance, however dramatic, doesn’t constitute a pattern. The company needs to demonstrate that Q1’s 5.2% net margin can hold or expand rather than revert toward the 0.8% level from a year ago, particularly if pricing pressure persists in the real estate sales segment that drives the majority of revenue.

What to Watch: The sustainability of net margins above 5% will determine whether Q1 represents a new baseline or an anomaly—monitor whether Q2 guidance materializes and if the Resort Operations segment can accelerate beyond 2.8% growth to diversify revenue drivers away from real estate sales concentration. The trajectory of VPG pricing and whether the 8% decline stabilizes or accelerates will signal pricing power in the core business. Credit quality metrics, particularly whether early-stage delinquencies maintain their four-year low, will validate the quality of contract sales growth. Finally, watch whether management can convert the $108.0M in free cash flow into shareholder returns or strategic investments that compound the margin expansion achieved in Q1.

This content is for informational purposes only and should not be considered investment advice. AlphaStreet Intelligence analyzes financial data using AI to deliver fast and accurate market information. Human editors verify content.

Source link

#Hilton #Grand #Vacations #Deep #Dive #EPS #Beats #Wide #Margin #Alphastreet