AlphaStreet Newsdesk powered by AlphaStreet Intelligence

Stock $17.13 (-5.9%)

EPS YoY -133.3%|Rev YoY -24.7%|Net Margin -1.3%

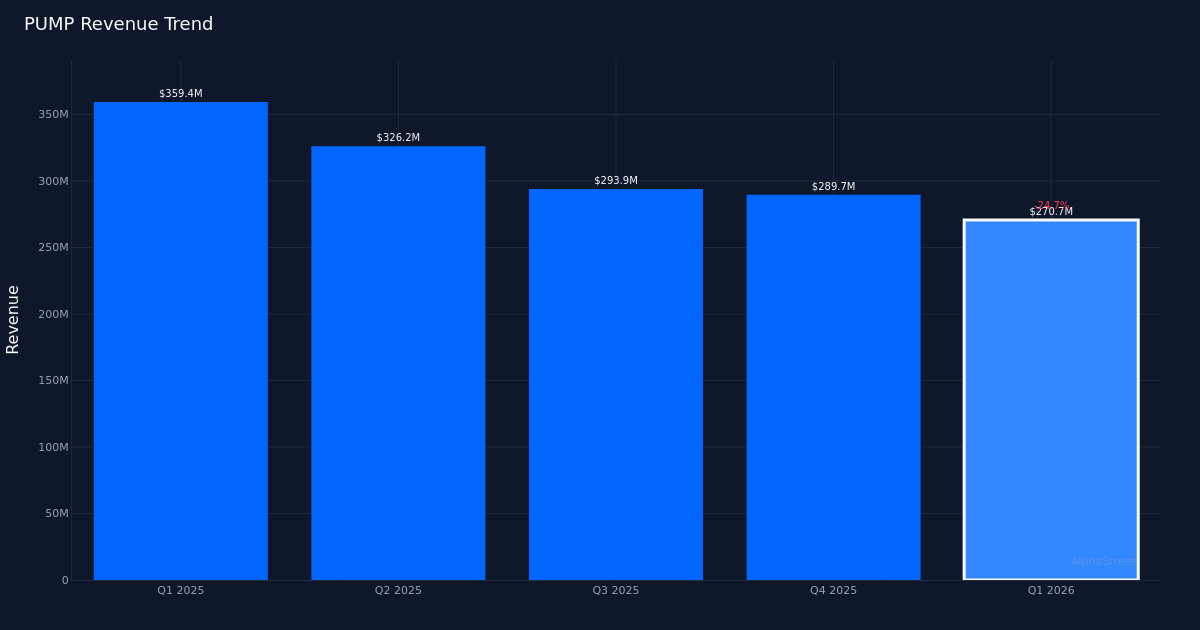

ProPetro delivered a narrower-than-expected loss but the quality of the result masks underlying deterioration across both the top and bottom lines. The oilfield services provider posted a loss of $0.03 per share in Q1 2026, beating analyst estimates by 70.0% against expectations of a $0.10 loss. Yet the stock tumbled 5.9% to $17.13 as investors looked past the beat to focus on deteriorating fundamentals: revenue plunged 24.7% year-over-year to $270.7M, marking the fourth consecutive quarterly decline, while the company swung from profitability to a loss position compared to the year-ago period when it earned $0.09 per share.

The earnings quality story reveals aggressive cost management compensating for weak pricing power and utilization. While ProPetro managed to post a modest $3.6M net profit despite revenue deterioration, margins compressed dramatically from year-ago levels. Net margin contracted by 4.0 percentage points to negative 1.3% from a positive 2.7% in Q1 2025, while operating margin sat at negative 3.0%. The company’s gross margin of 21.8% represents the first line of defense, but the compression at the operating level indicates that fixed cost leverage is working against management as revenue slides. Management noted that “net cash provided by operating activities was $3 million as compared to $81 million in the prior quarter,” highlighting the dramatic deterioration in cash generation from operations. The $36.4M in EBITDA provided some cushion, but adjusted EBITDA of 36.0 million dollars suggests limited room for further cost cuts without impairing operational capability.

The revenue trajectory points to sustained weakness in the hydraulic fracturing market that shows no signs of stabilizing. Sequential analysis of the four-quarter trend reveals a company in steady decline: from $326.2M in Q2 2025 to $293.9M in Q3, then $289.7M in Q4, and now $270.7M in Q1 2026. This represents a sequential decline of approximately 7%, consistent with management’s commentary that “during the first quarter, ProPetro generated total revenue of $271 million, a decrease of 7% as compared to the prior quarter.” The year-over-year comparison is even more sobering, with revenue down 24.7% from $359.4M in the prior-year quarter. This trajectory suggests the industry headwinds are intensifying rather than abating, with no inflection point visible in the current data.

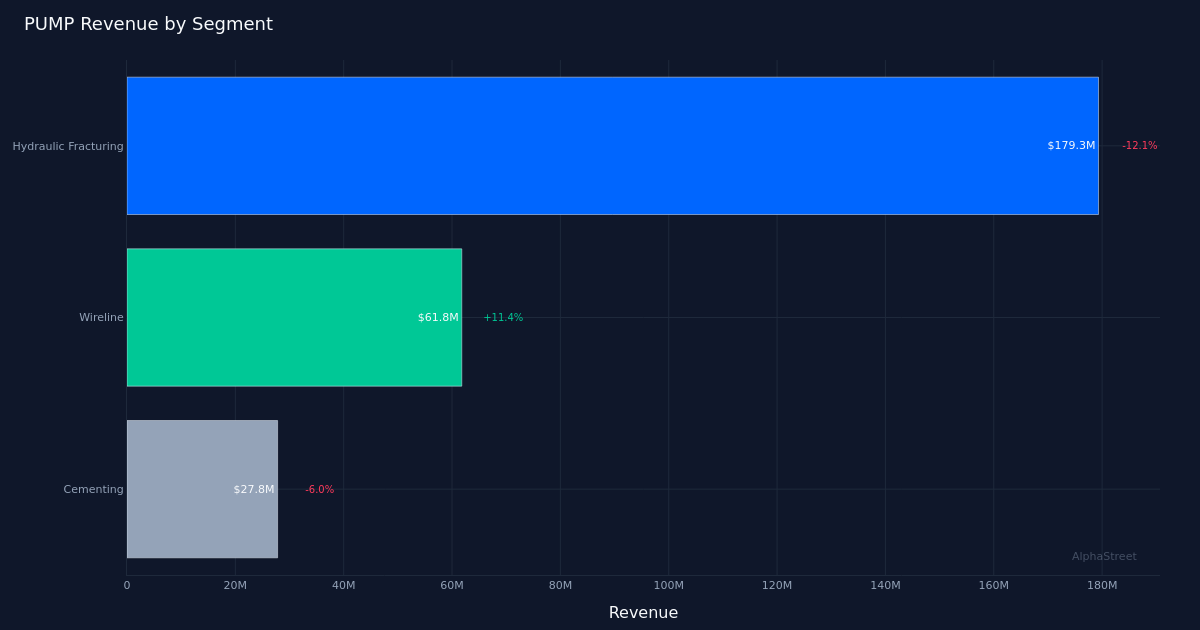

Segment dynamics reveal hydraulic fracturing weakness partially offset by wireline strength, but the core business remains under pressure. The hydraulic fracturing segment generated $179.3M with negative 12.1% growth, representing 66% of total revenue and serving as the primary drag on consolidated performance. This core business continues to face pricing pressure and utilization challenges characteristic of the broader North American completion services market. Wireline services provided a bright spot with $61.8M in revenue and positive 11.4% growth, demonstrating some pockets of demand strength. Cementing contributed $27.8M but declined 6.0%, suggesting the weakness extends beyond just hydraulic fracturing into other completion-related activities. The mixed segment performance indicates ProPetro isn’t simply facing company-specific execution issues but rather market-wide headwinds that are hitting its largest business the hardest.

Management’s focus on data center power generation projects signals a strategic pivot that won’t materially impact near-term results. The company disclosed updated equipment cost guidance “between 14 and 1,5 million per megawatt” for infrastructure projects supporting data centers, with total power generation capacity by year-end 2031 expected to reach 3 units. While this diversification into power generation for data centers represents a potentially meaningful long-term opportunity, the timeline extends through 2031, offering no relief for the current hydraulic fracturing downturn. Management’s speculative questioning about whether “a 5 to 10% gain in activity out there” would create “inflationary pressures on labor” suggests the company is gaming out modest recovery scenarios, but the hypothetical nature of the discussion underscores the absence of concrete signs of improvement in the current environment.

The earnings beat obscures the fact that ProPetro is managing decline rather than positioning for growth. While the company successfully controlled costs enough to beat lowered expectations, the 100% beat rate over the last quarter reflects analysts catching up to deteriorating fundamentals rather than the company outperforming. The $38.1M in free cash flow appears positive on the surface, but when contextualized against the mere $2.7M in operating cash flow, it suggests asset sales or working capital benefits that may not be sustainable. Management’s acknowledgement that adjusted EBITDA “decreased 29% compared to the prior quarter” frames the real story: this is a company experiencing margin compression, revenue erosion, and cash generation challenges despite beating lowered estimates.

The 5.9% stock decline reflects investor recognition that the beat was more about lowered expectations than operational improvement. The market’s negative reaction despite the earnings beat indicates that sophisticated investors are looking through the headline number to focus on the deteriorating revenue trend, margin compression, and absence of catalysts for improvement. The stock reaction suggests investors view the current quarter as another data point in a deteriorating trend rather than an inflection point toward recovery.

What to Watch: The key catalyst is whether Q2 2026 revenue can break the four-quarter decline trajectory or if the downward trend extends into a fifth consecutive quarter. Monitor hydraulic fracturing segment pricing and utilization trends, as stabilization in this core business is necessary before any sustainable recovery can begin. Watch whether operating cash flow can return to meaningful positive territory beyond the anemic $2.7M generated this quarter. Finally, track management’s progress on data center power generation contracts, as concrete project wins with specific megawatt commitments would validate the diversification strategy, though material revenue contribution remains years away.

This content is for informational purposes only and should not be considered investment advice. AlphaStreet Intelligence analyzes financial data using AI to deliver fast and accurate market information. Human editors verify content.

Source link

#ProPetro #Holding #EPS #Tops #Estimates #Deep #Dive #Alphastreet

plans. Should workers embrace them?")